Singapore Business Visa

Offshore services

Bundled Services

Top Citizenship & Residency

Articles & Research

About Us

Contact Us

.svg)

Trusted by Global Clients & Partners

July 7, 2026

6

min read

Dominica CBI for US Citizens 2026: Dual Citizenship, FATCA, and US Tax Guide

.svg)

2.6K

2.6K

Dominica Citizenship by Investment (CBI) is fully accessible to US citizens in 2026. Americans can apply from USD 200,000 via the Economic Diversification Fund (EDF) route, dual citizenship is permitted by both Dominica and the United States, and Dominica does not require applicants to renounce US citizenship. However, US citizens remain subject to US worldwide taxation under Citizenship-Based Taxation (CBT), FATCA reporting on foreign accounts, and the US Exit Tax under IRC Section 877A if they later renounce US citizenship.

Key Takeaways

- Dominica CBI is legal and accessible for US citizens. Americans can apply from USD 200,000 EDF, obtain a second passport in 6 to 9 months, and hold dual citizenship without renouncing US citizenship.

- US Citizenship-Based Taxation (CBT) still applies. American Dominica citizens continue to owe US federal tax on worldwide income and must file FBAR and FATCA reports on foreign accounts. CBI does not exempt US citizens from US tax obligations.

- Dominica does not hold a US E-2 Treaty. Americans seeking a US E-2 Treaty pathway for family members or non-US business partners should shortlist Grenada or St. Kitts and Nevis instead, both of which hold active E-2 treaties.

- Dominica passport adds Schengen Area, UK, Singapore, and Hong Kong to a US citizen's mobility. It does not add materially versus US passport for most global destinations, since the US passport already delivers 180+ visa-free destinations.

- Renunciation of US citizenship triggers the US Exit Tax under IRC Section 877A for covered expatriates (USD 2 million net worth or USD 200,000 average annual US federal tax liability). Renunciation is a serious step with permanent tax and mobility consequences.

Quick Facts: Dominica CBI for US Citizens 2026

Is Dominica CBI Legal and Accessible for US Citizens?

Yes. Dominica CBI is fully legal for US citizens and there are no US-citizen-specific restrictions in the program. Americans have applied to Dominica CBI in meaningful volume since the program's 1993 launch, and the CBIU processes US applications through the same framework as other nationalities.

Both countries permit dual citizenship. Dominica does not require applicants to renounce their original nationality. The United States permits US citizens to hold multiple citizenships without limitation. Approximately 15 to 20% of CBI applicants globally are US citizens, motivated by mobility diversification, tax planning setup, or Plan B insurance against domestic uncertainty.

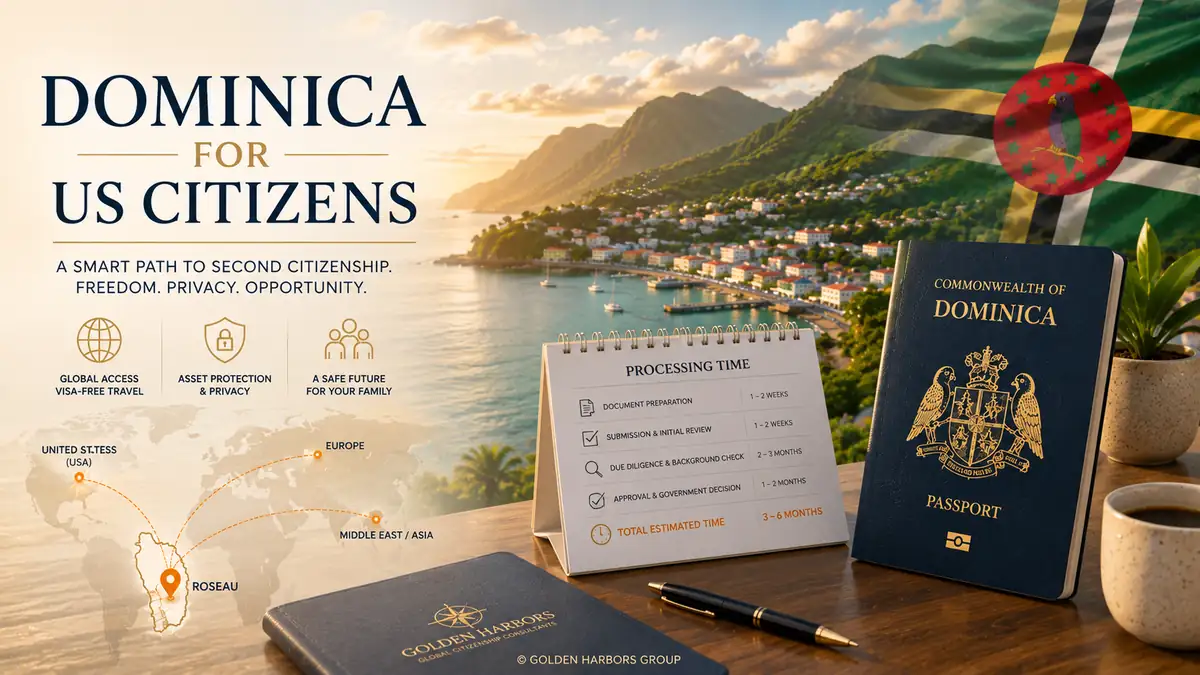

The Dominica CBI application from a US citizen follows the standard structure. The applicant retains a licensed CBIU agent, prepares the standard documentation package (passport, birth certificate, marriage certificate if applicable, FBI police clearance, medical certificate, 6 to 12 months of source-of-funds documentation, professional references), and submits through the licensed agent. Processing runs 6 to 9 months. For the full timeline breakdown, see the Dominica CBI processing time guide.

Under ECCIRA (operational Q2 2026), US applicants complete the mandatory virtual interview with biometric capture (fingerprints, facial recognition, digital signature) as part of the application. Biometric capture is conducted through approved digital platforms and does not require travel to Dominica.

Do US Citizens Still Pay US Tax After Getting Dominica CBI?

Yes. The United States taxes citizens on worldwide income regardless of second passport, second residence, or physical location. This is the US Citizenship-Based Taxation (CBT) rule, which applies to all US citizens including those who acquire additional citizenships through CBI. Dominica CBI does not reduce, eliminate, or affect US federal tax obligations.

Foreign Earned Income Exclusion (FEIE). Under IRC Section 911, US citizens who meet the bona-fide resident or physical presence test in a foreign country can exclude up to approximately USD 130,000 (2026 inflation-adjusted amount) of foreign earned income from US federal tax under the IRS Foreign Earned Income Exclusion. This exclusion is a US Internal Revenue Code provision, not a CBI benefit; it applies independently of Dominica citizenship.

Foreign Tax Credit (FTC). US citizens can claim a foreign tax credit for taxes paid to foreign jurisdictions on the same income. Dominica does not tax foreign-source income for tax residents (0% on foreign income), so US citizens do not accumulate Dominica-source foreign tax credits.

US worldwide tax rates apply. Federal income tax, self-employment tax, and Net Investment Income Tax (NIIT) continue to apply to worldwide income above the FEIE cap. Capital gains from any source remain subject to US federal capital gains tax at the applicant's US bracket rate.

The table below summarizes the US tax and reporting obligations that continue for a US citizen after acquiring Dominica CBI.

← Swipe →

| Obligation | Trigger | Form / Filing | Impact of Dominica CBI |

|---|---|---|---|

| Citizenship-Based Taxation | Being a US citizen | IRS Form 1040 (annual) | None. US federal tax on worldwide income continues. |

| FATCA reporting | Foreign accounts over USD 50K single / USD 100K MFJ | IRS Form 8938 (with 1040) | Applies to Dominica bank accounts opened after CBI. |

| FBAR reporting | Aggregate foreign accounts over USD 10K | FinCEN Form 114 (annual, April 15) | Applies to Dominica bank accounts. Separate from IRS. |

| Foreign Earned Income Exclusion | Bona-fide residence or physical presence abroad | IRS Form 2555 (with 1040) | Available; excludes ~USD 130,000 of earned income (2026). |

| Foreign Tax Credit | Foreign tax paid on same income | IRS Form 1116 (with 1040) | Limited use; Dominica taxes foreign income at 0%. |

| US Exit Tax (IRC 877A) | Renunciation + covered expatriate status | IRS Form 8854 + capital gains schedules | Triggered only if applicant renounces US citizenship. |

| US Estate Tax | US citizenship + worldwide assets over exemption | IRS Form 706 (estate) | None. US estate tax applies on worldwide assets. |

| Sources: IRS Foreign Earned Income Exclusion; IRS FATCA guidance; FinCEN FBAR guidance; IRS Expatriation Tax (IRC 877A). FEIE 2026 amount is inflation-adjusted per IRS revenue procedure. Covered-expatriate thresholds under IRC 877A: net worth USD 2 million or 5-year average annual US federal net income tax liability USD 200,000. This article is informational; verify current requirements with qualified US tax counsel before acting. | |||

Golden Harbors advisors coordinate with independent US tax counsel for cross-border structuring. We do not provide US tax advice directly. See the CBI FAQs pillar for the broader tax framework across all active CBI programs.

What Are the FATCA and FBAR Reporting Requirements?

US citizens with Dominica CBI face two ongoing US reporting requirements on their foreign financial accounts. Both are triggered by the existence of foreign accounts, not by CBI citizenship itself. CBI creates practical exposure by opening the door to Dominica banking relationships.

FATCA (Foreign Account Tax Compliance Act). Foreign financial institutions (including Dominica banks) are required to report US-owned account balances and income to the IRS annually under FATCA. Dominica financial institutions comply with FATCA through inter-governmental agreements between Dominica and the United States. US citizens with Dominica accounts are automatically reported through the institution; they must also file Form 8938 with their annual tax return if aggregate foreign account balances exceed the reporting threshold (USD 50,000 for single filers, USD 100,000 for married joint filers, higher for expatriates).

FBAR (Foreign Bank Account Report, FinCEN Form 114). US citizens with signature authority over or beneficial ownership of foreign accounts that exceed USD 10,000 in aggregate at any point during the calendar year must file the FBAR annually. FBAR is filed with FinCEN, separately from the IRS tax return, by April 15 (with automatic 6-month extension to October 15).

Non-compliance with FATCA or FBAR carries substantial civil and criminal penalties. Civil penalties for willful FBAR violations can reach the greater of USD 100,000 or 50% of the account balance per violation. Non-compliance is one of the most common enforcement priorities for the IRS Criminal Investigation division. US citizens with Dominica CBI should coordinate FATCA and FBAR compliance with their US tax preparer.

Does Dominica CBI Give US Citizens US E-2 Treaty Access?

No. Dominica does not hold a US E-2 Investor Visa Treaty. US citizens seeking to leverage a Caribbean CBI passport for E-2 Treaty pathway benefits should shortlist Grenada or St. Kitts and Nevis instead. This distinction is decisive for a specific use case and irrelevant for most US citizens.

Why E-2 matters. The US E-2 Treaty Investor Visa allows citizens of E-2 Treaty countries to live and work in the US through qualifying US business investment (typically USD 100,000 to USD 500,000 in an active US business the applicant controls). It is renewable indefinitely and can cover the applicant, spouse, and children under 21.

Why US citizens do not use E-2 directly. US citizens already have unrestricted US residence and work rights. E-2 is not for US citizens themselves. However, E-2 is highly valuable for family members or business partners who are non-US citizens and want US business access without the USD 800,000+ EB-5 commitment.

When to shortlist Grenada or St. Kitts instead of Dominica. If a US citizen's spouse, adult child, or key business partner is a non-US citizen who wants US operational rights via E-2, Grenada or St. Kitts CBI provides that pathway. Dominica does not. For a head-to-head between Dominica and St. Kitts including E-2 access as a decisive variable, see the Dominica vs St. Kitts comparison.

The table below compares the four leading Caribbean CBI programs plus Turkey for US citizens, with the US E-2 Treaty column highlighted as the decisive variable.

← Swipe →

| Program | Min. Investment (Single) | Timeline | Visa-Free | US E-2 Treaty | Best For |

|---|---|---|---|---|---|

| Dominica | USD 200,000 | 6 to 9 months | 145 destinations | No | Lowest cost; mobility only |

| Grenada | USD 235,000 | 6 to 8 months | 147 destinations | Yes | Non-US-citizen family needing E-2 |

| St. Kitts and Nevis | USD 250,000 | 4 to 6 months | ~150 destinations | Yes | Fastest OECS + E-2 access |

| Antigua and Barbuda | USD 230,000 | 6 to 8 months | 151 destinations | No | Strongest Caribbean passport |

| Turkey (non-Caribbean) | USD 400,000 (RE) | 3 to 6 months | ~120 destinations | Yes | E-2 + Middle East mobility |

| Sources: US Department of State E-2 Treaty Countries List; Dominica CBIU; IMA Grenada; St. Kitts and Nevis CIU; Antigua and Barbuda CIU; Turkey Ministry of Interior; Henley Passport Index 2026. E-2 Treaty status enables non-US-citizen family members or business partners to apply for the US E-2 Investor Visa; US citizens themselves have unrestricted US residence rights and do not use E-2 directly. All 4 Caribbean programs operate under ECCIRA harmonized standards from Q2 2026. | |||||

Turkey also holds a US E-2 Treaty. Applicants weighing E-2 pathway benefits alongside CBI can also consider Turkey CBI, though at a higher investment threshold (USD 400,000+ real estate).

What Does the Dominica Passport Add for US Citizens?

The Dominica passport delivers approximately 145 visa-free destinations (Henley Passport Index 2026, ranked 29th globally). The US passport delivers approximately 180 visa-free destinations (Henley Passport Index 2026, top-tier ranking). The overlap is substantial, so the Dominica passport's incremental mobility value for a US citizen depends on which specific destinations matter.

Destinations Dominica adds that US does not have visa-free. Certain destinations that require US citizens to obtain visas grant visa-free access to Dominica passport holders. The specific set varies by geopolitical bilateral relationships and changes periodically. See the Dominica passport visa-free countries guide for the current full list.

Destinations both passports serve. Schengen Area, United Kingdom, Singapore, Hong Kong, Japan, South Korea, most of Latin America and Southeast Asia are visa-free on both passports. The Dominica passport adds redundancy but no new access for these destinations.

Destinations US serves that Dominica does not. US passport visa-free access includes several destinations that require Dominica citizens to obtain visas. For frequent business travel to those specific destinations, the US passport remains the primary travel document.

Non-mobility value. The Dominica passport delivers additional value beyond visa-free counts: banking relationships in Caribbean and other 0% tax jurisdictions, standing in Commonwealth countries, an alternative document if the US passport is lost or restricted, and a Plan B citizenship in a politically stable jurisdiction. These are the primary drivers for most US citizens who acquire Dominica CBI.

How Should US Citizens Approach Renunciation and the Exit Tax?

Most US citizens who acquire Dominica CBI do not renounce US citizenship. Renunciation is a serious step with permanent consequences that most Americans avoid even after acquiring a second citizenship. However, ultra-high-net-worth Americans facing substantial cross-border tax friction sometimes consider renunciation after establishing tax residency in Dominica or another 0% tax jurisdiction.

US Exit Tax (IRC Section 877A). Renouncing US citizenship triggers Exit Tax for "covered expatriates": US citizens who meet either of two thresholds at renunciation under the IRS Expatriation Tax rules. First, net worth of USD 2 million or more at the date of renunciation. Second, average annual US federal net income tax liability of USD 200,000 or more (adjusted for inflation) for the five taxable years ending before the renunciation date. Covered expatriates are treated as having sold their worldwide assets at fair market value on the day before renunciation, with capital gains tax due on the deemed sale.

Exit Tax exemption. An initial exclusion applies (approximately USD 890,000 for 2026, inflation-adjusted) before Exit Tax computation. Above the exclusion, standard federal capital gains rates apply (up to 20% for high-income taxpayers, plus 3.8% Net Investment Income Tax).

Post-renunciation consequences. After renunciation, the former US citizen loses US visa-free travel to many countries, faces potential entry restrictions to the United States, and cannot vote in US federal elections or receive US federal benefits. Renunciation is administratively difficult (in-person appointment at a US consulate abroad, USD 2,350 renunciation fee, and 6 to 12 month processing timeline) and legally permanent.

Practical guidance. Most US citizens acquiring Dominica CBI treat it as a supplementary citizenship, not a substitute for US citizenship. Renunciation planning, when relevant, is typically undertaken with US tax counsel over a 2 to 5 year horizon and combines Dominica CBI or another 0% tax citizenship with structured wealth transfer and tax residency migration before the renunciation date. Golden Harbors does not provide US tax advice; we coordinate with US tax counsel through our referral network.

How Do US Citizens Apply From Inside the United States?

Dominica CBI applications from US citizens follow the standard remote-filing framework. No travel to Dominica is required for the application itself. The full process runs through a licensed CBIU agent and can be completed from any location in the United States.

FBI police clearance. US citizens obtain the FBI Identity History Summary Check (also known as FBI police clearance) through the FBI Criminal Justice Information Services (CJIS) division. Processing runs 4 to 8 weeks for standard requests; expedited requests through third-party channelers can compress to 1 to 3 weeks. Every jurisdiction of residence in the past 10 to 15 years also requires state-level or local police clearance. The FBI clearance must be dated within 6 months of application submission.

US-based biometric capture. Under ECCIRA, biometric capture (fingerprints, facial recognition, digital signature) is required for the mandatory virtual interview. Approved digital platforms permit biometric collection from any US location without requiring in-person visits to a Dominica-affiliated venue.

Source of funds documentation. US applicants document source of funds through 6 to 12 months of bank statements, US federal tax returns (IRS Form 1040 for the past 2 to 3 years), employment or business records, and any relevant investment or asset documentation. All documents must be certified copies where the CBIU requires originals.

Investment payment. The USD 200,000 EDF contribution is wired from a US bank account to the CBIU escrow account. US wire transfer rules and Bank Secrecy Act reporting requirements apply. Wires over USD 10,000 are reported through standard IRS Currency Transaction Reports; wires over USD 3,000 include enhanced Know Your Customer documentation at the US originating bank.

Oath of allegiance. The oath is sworn at a Dominica embassy or honorary consulate. The Dominica High Commission in New York and Dominica consular offices in Washington DC and Miami serve US applicants. Alternatively, the oath can be sworn at approved venues abroad if the applicant is traveling internationally.

Frequently Asked Questions

Can US Citizens Legally Apply for Dominica CBI?

Yes. Dominica CBI is fully legal for US citizens. The Dominica CBIU accepts applications from US citizens on the same terms as other nationalities, and the US does not restrict US citizens from acquiring second citizenships through investment programs. Approximately 15 to 20% of global CBI applicants are US citizens seeking mobility diversification, tax planning setup, or Plan B insurance.

Do I Have to Pay Taxes in Dominica if I Get CBI?

Not automatically. Dominica CBI grants citizenship but not tax residency. Tax residency requires meeting Dominica's separate tax residency rules (typically 183+ days per year of physical presence, or center of vital interests). Non-resident US citizens with Dominica CBI have no Dominica tax obligation. Tax residents pay 0% on foreign-source income; domestic-source income is taxed at standard local rates.

Will FATCA Reporting Change If I Get Dominica CBI?

Not directly. FATCA reporting is triggered by the existence of foreign financial accounts, not by CBI citizenship. US citizens who open Dominica banking accounts (a common downstream step after CBI) trigger FATCA reporting through those accounts. Dominica financial institutions comply with FATCA through inter-governmental agreements with the US. The applicant must also file Form 8938 with the annual US tax return.

Does Dominica CBI Grant US Business Access?

No. Dominica does not hold a US E-2 Investor Visa Treaty. US citizens seeking to leverage a Caribbean CBI passport for E-2 Treaty pathway benefits (typically for non-US-citizen family members or business partners) should shortlist Grenada or St. Kitts and Nevis instead, both of which hold active E-2 treaties. Turkey CBI also grants E-2 access at a higher investment threshold.

Can I Renounce US Citizenship After Getting Dominica CBI?

Yes, but with substantial tax and administrative consequences. Renunciation triggers the US Exit Tax under IRC Section 877A for covered expatriates (USD 2 million net worth or USD 200,000 average annual US federal tax liability). Renunciation is legally permanent, requires in-person appointment at a US consulate abroad, costs USD 2,350, and takes 6 to 12 months to process. Most US citizens acquiring Dominica CBI retain US citizenship.

Do American Family Members Also Get Dominica Citizenship?

Yes. Dominica CBI includes spouse, dependent children up to age 25 in full-time education, and dependent parents and grandparents (55+) in a single application. Every included family member acquires Dominica citizenship independently and can pass it to descendants by jus sanguinis. American family members already US citizens can hold both citizenships without restriction. Family inclusion fees apply per additional dependent.

How Golden Harbors Helps US Citizens With Dominica CBI

Golden Harbors advisors work with US citizens acquiring Dominica CBI through licensed CBIU agents, coordinating documentation preparation, FBI police clearance timing, source-of-funds packaging, and US-based biometric capture for the ECCIRA mandatory interview. We coordinate with independent US tax counsel through our referral network for FATCA compliance, US worldwide tax planning, and, where applicable, renunciation and Exit Tax structuring.

For US citizens weighing Dominica against Grenada or St. Kitts (the two E-2 Treaty Caribbean CBIs), see the Dominica vs St. Kitts comparison. For total-cost benchmarking across the Caribbean cluster, see the cheapest Caribbean CBI comparison. For a full timeline and due diligence breakdown, see the Dominica CBI processing time guide and the Dominica CBI due diligence guide. For the underlying program mechanics, see the Dominica CBI guide.

Ready to move from research to action? Book a general consultation call with Golden Harbors, global mobility experts who walk you through Dominica CBI for US citizens, FATCA and CBT implications, and E-2 Treaty alternatives for your family situation.

Book a CallAbout the Author

Victoria Cold, European Attorney at Golden Harbors, is an international lawyer and author of academic papers on corporate and immigration law. She holds multiple law degrees and speaks four languages, with deep coverage across Europe, the Middle East, and Asia. At Golden Harbors, she advises entrepreneurs, family offices, and international clients on cross-border structuring, residency, and citizenship-by-investment programs.

Last reviewed: July 2026.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or immigration advice. Program terms, tax rates, and regulatory requirements change frequently. Verify current requirements before acting.

There are Always Options to EXPAND YOUR BOUNDARIES! Let's Discuss Yours

Every client is unique

Every case requires an individual approach and solution. Our years of experience in the industry allow us to provide both.

We will answer all your questions and provide detailed information about the available second passport and residency programs to help you make the right choice.

Victoria

Lead Attorney at Golden Harbors

Victoria

Lead Attorney at Golden Harbors

Read also